Think a declined card transaction just means a missed sale?

Think again.

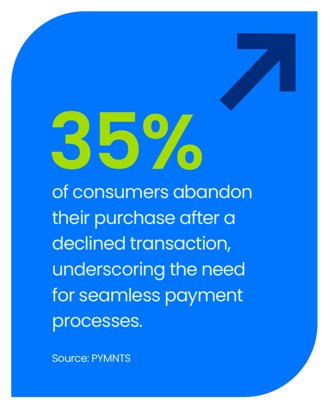

While an issuer decline may not be your company’s fault, late or missed shipments caused by payment failures can leave customers wondering if your business is reliable and can have them looking at your competitors.

We’ll cover five common reasons card issuer rejections happen and the steps you can take to manage them to reduce churn and keep your customers happy.

But, not all declined transactions are created equal.

Understanding why card issuer declines happen is the first step toward managing them effectively.

What does card declined by issuer mean?

If you have a credit or debit card, you’re familiar with card issuers. Think banks like JPMorganChase, Bank of America and Citibank, as well as credit unions and prepaid card providers.

These issuers — also known as issuing banks — are financial institutions that provide payment cards to consumers and businesses, such as credit cards, debit cards and prepaid cards.

From insufficient funds to suspected fraud, an issuer rejection can occur for a number of reasons. But, at this point, the issuer has put a stop to the transaction.

When a card has an unsuccessful charge, the merchant usually receives an issuer decline code and a brief explanation.

Two types of declines

Card declines generally fall into two categories — hard declines and soft declines — each requiring a different approach to recovery.

- Hard declines are permanent payment failures. Retrying these transactions on the same card won’t result in payment success. You’ll need to get new payment details from the customer.

- Soft declines are temporary payment failures. If you can pinpoint the error behind them, you can take steps to overcome it and likely see the transaction succeed.

Merchants can reduce the likelihood of declines happening in two ways:

- First, by implementing decline management processes to cut down on payment failures.

- Second, by automating alerts or creating another system that communicates errors to customers in time for them to update their payment information.

With this in mind, let’s explore the leading causes ecommerce merchants face credit card issuer rejections — and proven strategies to overcome them.

1. Incorrect credit card details

One of the main reasons why issuer declines happen — and thankfully, one of the easiest to fix — is incorrect billing information. A typo in the account number or an incorrect CVV code can cause a denial because the card issuer could not match the input to an account in its system.

These are classified as hard declines, meaning customers must update their payment information or use a different payment method to proceed.

How to fix it

The best approach to address this issue is to make the process of fixing the card error as simple as possible for the customer. Removing as many hurdles as possible will result in fewer customers bouncing when they’re hit with this type of declined payment.

- Be specific in your error messages: Indicate the specific reason for the payment failure, whether it's an invalid credit card number, a misspelled name or a CVV mismatch. This transparency gives customers a sense of control and helps them resolve the issue faster.

- Streamline the update process: Allow customers to edit their billing details quickly and retry the transaction. The more seamless the process, the less likely they are to abandon their purchase.

- Offer alternative payment methods: If they can’t resolve the error, give customers the option to easily switch to another digital wallet, such as Google Pay, Apple Pay or PayPal. A single click to add or update a payment method can significantly improve your conversion rates.

2. Insufficient funds or credit limit reached

Issuing banks often decline transactions when a customer exceeds their credit limit, daily spending limit or withdrawal maximum. This can be a sensitive issue because it may signal that the customer is having financial troubles.

Thankfully, these are soft declines, meaning you may be able to get the transaction approved without involving the customer at all.

How to fix it

There are several ways you can address this error.

- Offer alternatives immediately: When the error occurs during a live transaction, inform the customer of the issue and guide them to complete their purchase with a different payment method. Options like buy now, pay later (BNPL) can be particularly helpful for customers with temporary financial constraints.

- Keep it low effort: Ideally, avoid placing too much responsibility on the customer, as high-effort solutions (e.g., telling them to call their bank) often lead to cart abandonment. You won’t be able to accomplish this in every scenario, but whenever possible, look for ways to take the onus off your customer.

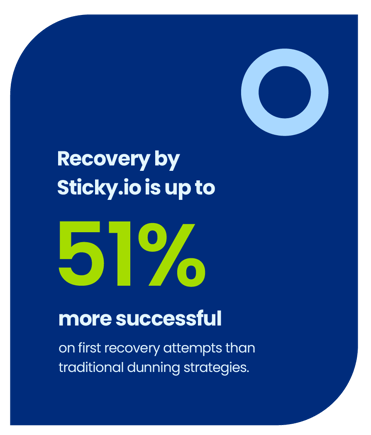

- Use automated retries: Tools like Sticky.io’s Recovery automatically retry payments after a temporary decline, taking the guesswork out of rebilling and improving involuntary churn and revenue recovery.

- Set up smart notifications: If retries fail, notify customers promptly and explain the next steps. Transparency reduces frustration and sets realistic expectations for the customer, like when they can expect their next shipment.

- Offer flexible options: Provide customers with the ability to switch payment methods on file or adjust their billing dates to align with their financial situation.

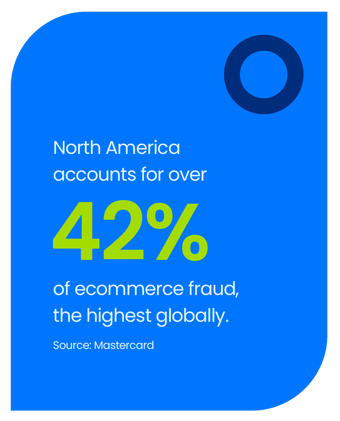

3. Suspected fraud

Card issuers may reject a transaction if the account is flagged for fraud or suspicious activity, such as unusual spending patterns or potential unauthorized purchases.

Advanced fraud detection systems, while effective, can sometimes mistakenly flag legitimate transactions as suspicious, leading to declines. This is often referred to as a "false decline."

Fraud is always classified as a hard decline because credit card issuers prioritize protecting their customers from unauthorized transactions. While frustrating, this type of payment failure is often resolvable with proper communication and guidance.

How to fix it

When a transaction is declined for issuer suspected fraud, the approach to resolve it will vary depending on whether it’s a one-time purchase, a recurring transaction or a false decline.

For one-time payments:

- Notify the buyer promptly: Inform customers that their transaction was flagged as fraud and suggest they verify their billing information, such as their ZIP code or CVV, to rule out minor errors.

- Have customers contact their bank: If no errors are found, customers will need to contact the financial institution directly to resolve the problem and authorize the transaction. Let the customer know they’ll need to provide their bank with details of the flagged purchase (amount, merchant name, date) to make this process easier for them.

For subscription payments:

- Investigate payment processing changes: Recurring payments may be flagged if your payment processor has made changes, such as switching banks or locations. For example, crowdfunding platform Patreon experienced increased fraud reports after moving to a Dublin-based bank.

- Offer flexible solutions: Ask customers to use a different card if their current one continues to be declined. Alternatively, suggest they retry the transaction after contacting their bank to authorize it.

For false declines:

- Optimize your fraud prevention settings: Regularly review and adjust your fraud detection parameters to minimize false positives.

- Implement advanced fraud detection tools: Use machine learning-based systems that can better distinguish between fraudulent and legitimate transactions.

- Provide clear communication: Inform customers about unsuccessful transactions due to security checks and offer options to verify their identity if necessary.

- Monitor decline reasons: Analyze decline codes to identify common issues and address them proactively.

4. Lost or stolen card

Card issuers will reject any transaction charged to a card reported as lost or stolen.

These are hard declines, meaning the transaction cannot be processed without obtaining a different payment method from the customer.

How to fix it

When a card is reported as missing or compromised, it’s essential to act quickly to minimize disruption for both your customer and your business. Here are several strategies to do just that:

- Notify the customer immediately: Inform the customer that their card has been reported as compromised and ask them to provide an alternative payment method.

- Monitor for fraud: While most buyers are aware of reporting their card as lost or stolen, unusual behavior (e.g., a lack of awareness or urgency) may signal fraud. Kount’s anti-fraud suite or similar tools can look for suspicious activity that denotes a buyer as a scammer.

- Set up automated reminders: Customers may not recall every account their card is used on. Or they may forget to update their account as they manage everything that comes with a missing or stolen card. To help your customers manage this, use automated dunning emails to remind them to update their payment information.

- Offer seamless payment updates: To minimize friction for your customers and reduce churn for your business, provide an easy-to-use portal or link within your dunning email for customers to update their payment method.

5. Card has expired

Most credit cards are valid for three to five years, so a portion of your returning customers or subscribers will inevitably need to update their card information.

Purchases attempted on an expired card are classified as hard declines because the credit card company won’t recognize the card as valid, meaning customers must update their payment info or use a different payment method to proceed.

How to fix it

Expired cards are a common issue but can be resolved with proactive communication and a streamlined process. By making it easy for customers to update their payment information and leveraging automation tools, you can reduce transaction failures and improve customer retention.

Streamline your process:

- Address input errors: If a customer misenters the expiration date, prompt them to double-check and reenter the correct details.

- Improve user experience: For customers attempting to use an expired card, provide a simple, streamlined process to input new credit card information. Ideally, allow them to update their payment details without redirecting to another page to minimize friction.

Implement proactive measures:

- Use an Account Updater service: You can help prevent expired card errors on your recurring transactions by investing in tools like an Account Updater to automatically request updated payment information from issuing banks.

- Proactively notify customers: If you don’t have an Account Updater, set your system to flag cards that will expire within 30–60 days. Then, send reminders to those flagged accounts, prompting them to update their payment details before the expiration date. Most issuers send replacement cards one to two months before expiration, giving customers time to update their payment method.

- Be clear and proactive in your messaging: For example: “We noticed your card on file will expire soon. Update your payment details now to avoid any interruptions to your subscription or service.”

Decoding and resolving other card issuer rejections

While the five scenarios above address the top causes for card issuer rejections, there are many other potential causes. Each failed transaction is accompanied by a two-digit credit card decline code, which can help you identify the issue and determine steps to address it.

When you need to involve the customer, provide clear and actionable information to help them understand the problem and how to fix it. Payment errors can create frustration or financial anxiety, so transparent communication is critical to preserving trust and retaining your customers.

The best way to prevent churn is to minimize card issuer rejections from the start. Merchants should consider implementing the following tools and best practices, including:

- A robust decline management tech stack: Solutions like Sticky.io’s Recovery, Account Updater and advanced anti-fraud tools can help you minimize payment failures.

- PCI compliance: Ensure your site meets all PCI standards to protect sensitive payment information.

- Authentication tools: Add features like 3D Verify to improve transaction security and reduce chargebacks.

- Tokenization and encryption: Employ security measures to protect customer payment data and reduce the risk of rejections.

Card refusals don’t just disrupt payments — they can harm the strong relationships you’ve built with your customers. By implementing the tools and strategies outlined here, you’ll reduce card issuer rejections, prevent unnecessary churn and foster long-term loyalty.

The Credit Card Decline Code Cheat Sheet

Learn what the most common decline codes mean and how you should respond. Download now for free!