Between friendly fraud, rising dispute volumes, false declines, and new compliance programs like Visa’s Acquirer Monitoring Program (VAMP), modern merchants are facing pressure from every direction. A single spike in disputes can impact profitability, damage merchant account health, increase processing costs, and in severe cases, threaten a business’s ability to process payments altogether.

For subscription and ecommerce brands, chargebacks are no longer just a customer service issue. They’re a revenue operations issue.

This Guide Breaks Down:

- What chargebacks are and why they happen

- How chargeback ratios work

- Why Visa’s VAMP program changes the stakes for merchants

- The biggest causes of disputes and friendly fraud

- Proven strategies to prevent chargebacks before they happen

- How alerts, representments, routing, and recovery tools help reduce revenue leakage

Whether you’re trying to lower disputes, improve merchant account health, or protect recurring revenue, this guide will help you build a smarter chargeback prevention strategy.

What is a Chargeback?

Chargebacks were introduced decades ago to help consumers feel safe using credit cards. At the time, the system made perfect sense. Cardholders needed reassurance that fraudulent purchases wouldn’t leave them financially responsible.

Fast forward to modern ecommerce, and the landscape looks very different.

Today, chargebacks have evolved from a consumer protection mechanism into a growing operational challenge for merchants, especially ecommerce and subscription businesses processing high volumes of card-not-present transactions.

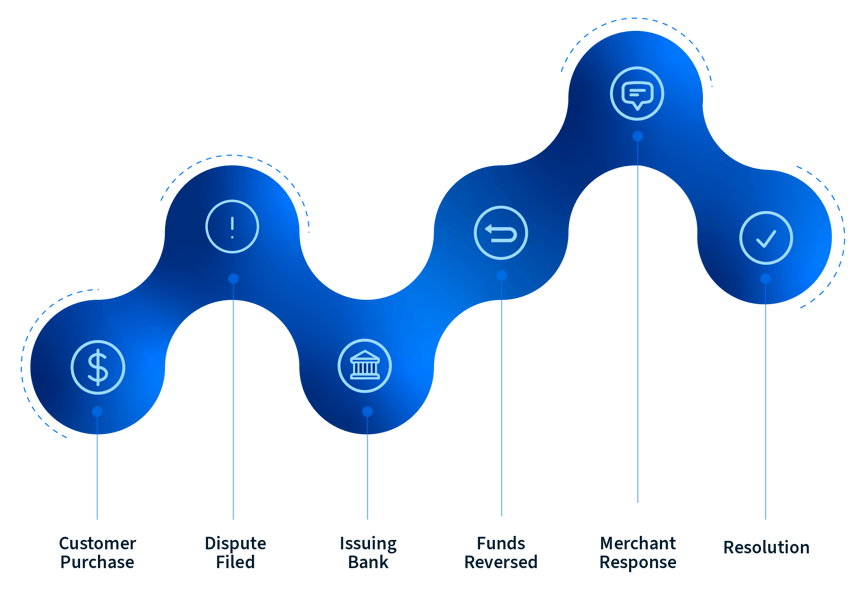

A chargeback occurs when a customer disputes a transaction with their issuing bank instead of requesting a refund directly from the merchant. Once initiated, the issuing bank reverses the transaction while investigating the claim.

If the merchant loses the dispute, they often lose:

- The original transaction revenue

- The product or service delivered

- Chargeback fees

- Additional operational costs tied to investigation and resolution

And increasingly, merchants are losing disputes tied not to true fraud, but to customer behavior.

This is why chargebacks can quickly become a problem for ecommerce merchants who haven’t created processes to prevent and address them. Prevention comes first, but you also must know how to complete the representments process to challenge chargebacks your company believes were wrongly filed.

How the Chargeback Process Works

The typical chargeback flow looks like this:

- A customer disputes a charge with their bank

- The issuer receives the dispute and pulls the transaction data from its record to investigate the purchase

- The issuer informs the merchant they’ve had a chargeback filed against them

- The merchant can either accept the dispute or fight it through representment

- The issuer makes a final ruling

If at step four, the merchant chooses to dispute the chargeback, the steps that follow include:

- The merchant gathers evidence showing the customer’s chargeback request should not be honored and submits it to the issuer for review

- The issuer reviews evidence from both sides and determines whether to award the chargeback or reject the claim

- A merchant who loses must refund the customer and pay chargeback fees

- If the merchant and issuing bank cannot agree on whether the charge should be paid, the case will go to arbitration

In many cases, merchants begin at a disadvantage because the burden of proof falls on them to demonstrate the transaction was legitimate.

The chargeback process may take upward of a few months, and each chargeback takes hours to fight. Merchants who receive more than a few chargebacks each month may see a significant amount of their resources go toward fighting chargebacks and paying fees.

Chargebacks vs Refunds

Refunds happen directly between merchants and customers.

Chargebacks involve banks, processors, card networks, fees, and compliance thresholds.

That distinction matters because chargebacks have downstream consequences far beyond the lost transaction itself. Excessive disputes can impact processor relationships, trigger monitoring programs, increase reserve requirements, and raise transaction costs.

Chargebacks vs Voided Transactions

A voided transaction doesn’t involve money changing hands because it’s canceled before it settles — meaning the funds aren’t credited to your account and then returned to a customer’s account. Both you and the buyer may see the transaction as pending in your accounts, but it’s never completed.

The timeline for a voided transaction is shorter, as most transactions are completed within a day or two of the purchase date. Because a transaction can only be canceled before it settles, this corrective measure is typically used for obvious mistakes (like double charges) that can be seen when a transaction posts. They’re not typically used to handle product-related complaints because ecommerce merchants don’t usually deliver goods until after a transaction has settled.

The Rise of Friendly Fraud

Not all chargebacks stem from stolen cards or criminal fraud.

This kind of fraud occurs when legitimate customers dispute valid transactions. Sometimes this happens accidentally due to confusion around billing descriptors or recurring subscriptions. Other times, it’s intentional.

Industry research estimates that 60–80% of chargebacks may now fall into the friendly fraud category.

For subscription brands, common triggers include:

- Forgotten subscriptions

- Trial-to-paid confusion

- Delayed cancellations

- Family member purchases

- Dissatisfaction with product expectations

The result is the same: lost revenue, operational strain, and growing compliance risk.

Why Chargebacks Matter More Than Ever

Chargebacks have always been expensive. But in modern ecommerce, they’ve become significantly more dangerous because they now impact everything from customer retention to processor relationships.

According to industry estimates, chargebacks cost businesses billions annually through lost revenue, fees, labor costs, and fraud exposure.

And the financial impact extends far beyond the disputed transaction itself.

The Real Cost of Chargebacks

Every chargeback creates multiple layers of cost:

- Lost merchandise or services

- Processor penalties and fees

- Manual review labor

- Customer support costs

- Shipping losses

- Increased fraud monitoring requirements

- Higher reserve requirements

- Lost customer lifetime value

For subscription businesses, the impact compounds quickly because a single dispute can terminate an otherwise valuable recurring customer relationship.

Why Subscription Businesses Face Higher Risk

Subscription ecommerce introduces unique dispute challenges:

- Recurring billing cycles

- Automatic renewals

- Trial offers

- Upsells

- Rebill confusion

- Failed payment retries

Customers may forget they subscribed, misunderstand billing schedules, or dispute transactions after failed cancellation attempts.

At the same time, subscription merchants often process higher transaction volumes, increasing exposure to dispute thresholds and monitoring programs.

How Chargebacks Impact Merchant Account Health

Processors and acquiring banks closely monitor dispute activity because excessive chargebacks signal elevated risk.

High dispute levels can lead to:

- Increased processing fees

- Reserve requirements

- Processor scrutiny

- Frozen funds

- MID termination

- Placement into card network monitoring programs

That’s why chargeback prevention is no longer just about fraud mitigation. It’s about protecting long-term payment stability and revenue continuity.

What Is a Chargeback Ratio?

A chargeback ratio is one of the most important metrics payment processors and card networks use to evaluate merchant risk.

At its simplest, a chargeback ratio compares the number of chargebacks a business receives against the number of transactions it processes.

Your ratio is always determined by the number of chargebacks in relation to the total number of transactions, regardless of the dollar amounts involved. A chargeback over a $1.99 purchase will affect your chargeback ratio the same way a chargeback over a $1,999 purchase would. And your chargeback ratio counts every payment dispute filed against your business, regardless of the outcome of any representment case. If a chargeback was filed, it’s included in the ratio.

How Chargeback Ratios Are Calculated

The basic formula looks like this:

Chargebacks ÷ Total Transactions = Chargeback Ratio

For example:

- 100 chargebacks

- 10,000 transactions

- = 1% chargeback ratio

However, the number you get from this formula won’t be exactly what card issuers are looking at.

Each card issuer looks only at the sales made on its network. Therefore, if you made 500 sales and received four chargebacks, you’d have a ratio of .8% — below the threshold for both Visa and Mastercard. However, if 350 of those sales and all four of those chargebacks were on Visa cards, Visa would calculate your chargeback ratio as 1.1%. Mastercard, meanwhile, would believe your chargeback ratio was 0%. In this case, your chargeback volume wouldn’t be high enough to trigger action from Visa, but higher-volume sellers with an acceptable overall chargeback ratio may find themselves breaching a card’s threshold because of this variation.

There’s one other quirk in this calculation: Mastercard looks at the number of chargebacks filed against you this month, but the number of sales you made last month. That means businesses with high fluctuations in sales volume may see their chargeback ratio skyrocket when entering a period of rapid growth after a spell of stagnation.

Different card networks calculate ratios differently, but the principle remains the same: higher dispute rates indicate greater merchant risk.

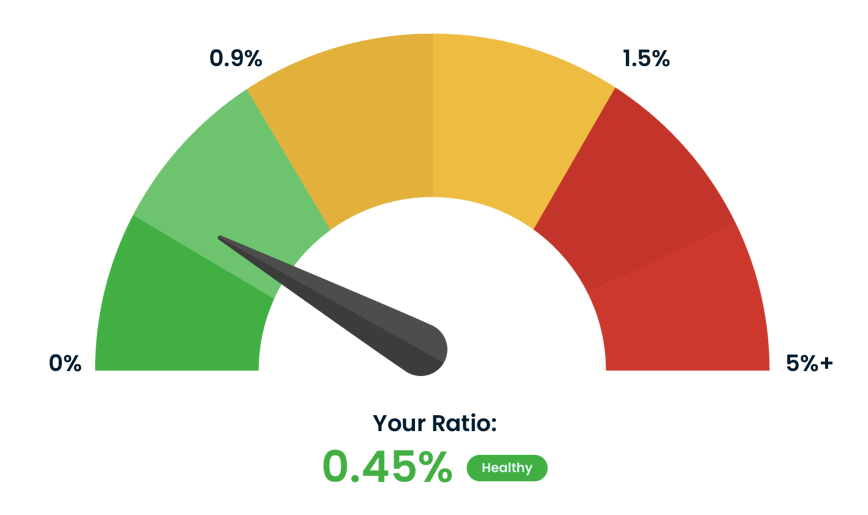

What Is Considered a High Chargeback Ratio?

Generally:

- Below 0.9% is considered healthy

- Ratios approaching 1% may trigger increased scrutiny from processors or card networks

- Excessive ratios can lead to monitoring programs or penalties

Merchants who have a high chargeback ratio may struggle to find financial partners and will almost certainly end up paying higher fees. They may also have to work with resource-intensive restrictions. Sellers who reach the threshold for “excessive” chargebacks will be categorized as high-risk.

These businesses will have to find payment processors willing to open a high-risk merchant account for them. A high-risk account typically charges higher interchange and chargeback fees. You may also have to pay a monthly fee and participate in costly risk monitoring programs.

If your chargeback ratio gets high enough, you may simply have your merchant account closed and your merchant ID revoked.

Visa, Mastercard, and acquiring banks all maintain their own thresholds and enforcement standards.

Visa’s legacy dispute monitoring thresholds have evolved under the Visa Acquirer Monitoring Program (VAMP), which now evaluates fraud and dispute activity through a combined card-not-present monitoring framework.

For example: Mastercard gives sellers more leeway than Visa. Merchants aren’t placed in the excessive category unless they have more than 100 chargebacks filed against them each month and a chargeback ratio of 1.5%. Its threshold for high excessive chargebacks is 1,000 per month and a rate of 3%. Businesses in either of these categories must pay monthly fines that start at $1,000.

Why Chargeback Ratios Matter

Chargeback ratios directly influence:

- Merchant account stability

- Processor relationships

- Reserve requirements

- Processing costs

- Compliance exposure

High ratios can limit a business’s ability to scale efficiently.

For subscription merchants, maintaining healthy ratios is especially important because recurring billing naturally creates additional dispute exposure.

Common Causes of Rising Chargeback Ratios

Several operational issues can increase dispute volume:

- Friendly fraud

- Shipping delays

- Poor customer support

- Billing descriptor confusion

- Failed payments

- Affiliate fraud

- Subscription cancellation friction

- Product expectation mismatches

Understanding which operational areas contribute most heavily to disputes is critical for long-term prevention.

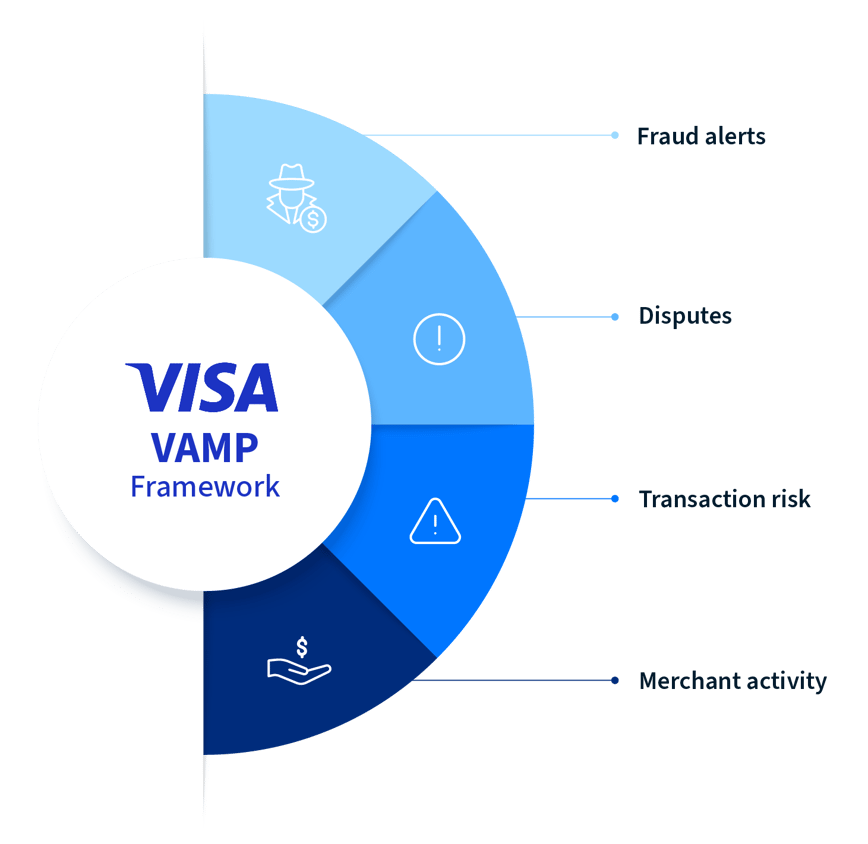

Visa’s New VAMP Program Is Changing the Rules

Visa’s Acquirer Monitoring Program (VAMP) is reshaping how merchants think about chargebacks, fraud, and payment performance.

Instead of treating fraud alerts and disputes separately, Visa now evaluates merchants using a more unified risk framework that combines fraud and dispute activity together.

For ecommerce and subscription brands, the implications are significant.

Chargeback prevention is no longer just about recovering revenue. It’s about protecting your ability to process payments efficiently at scale.

For a deeper breakdown, explore our guide to Visa’s Acquirer Monitoring Program (VAMP) or review our glossary definition of what VAMP means for merchants.

How VAMP Changes Merchant Risk

Under VAMP, even moderate increases in fraud or disputes can create downstream risk for merchants and processors.

That means businesses may face:

- Increased scrutiny from acquiring banks

- Higher reserve requirements

- Processor intervention

- Additional compliance monitoring

- Potential fines or penalties

Subscription businesses processing high recurring transaction volume are especially vulnerable because even small percentage increases can scale quickly.

VAMP also increases accountability for acquiring banks and payment processors, which means merchants with elevated dispute activity may face stricter oversight from their payment partners.

Why Subscription and Ecommerce Brands Are Most Vulnerable

Card-not-present transactions naturally carry higher fraud and dispute exposure.

Add recurring billing into the mix, and the risk profile increases further.

Common risk drivers include:

- Trial-to-paid confusion

- Forgotten subscriptions

- Failed payment retries

- Cross-border transactions

- Billing misunderstandings

- High-volume rebills

VAMP places additional pressure on businesses to proactively manage these operational risks before disputes escalate.

What Happens If Your Business Exceeds VAMP Thresholds?

Merchants with elevated fraud or dispute activity may face increased scrutiny from processors and acquiring banks, potentially leading to:

- Additional monitoring

- Reserve requirements

- Financial penalties

- Fund holds

- MID restrictions

- Account termination risk

That’s why proactive dispute reduction strategies matter more than ever.

How to Stay Below VAMP Thresholds

Under VAMP, prevention matters more than recovery. Reducing disputes before they formally escalate is often more impactful than fighting them after the fact.

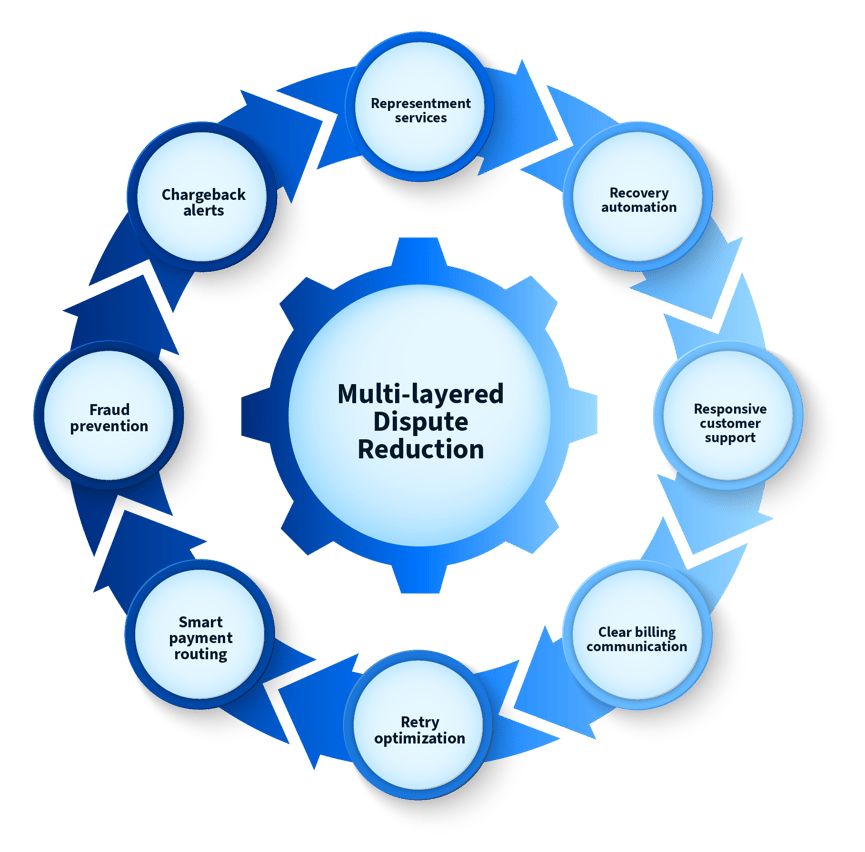

Reducing disputes requires a multi-layered approach:

- Chargeback alerts

- Fraud prevention

- Smart payment routing

- Retry optimization

- Clear billing communication

- Responsive customer support

- Recovery automation

- Representment services

The goal isn’t just fighting disputes after they happen. It’s reducing the likelihood they happen in the first place.

The Most Effective Chargeback Prevention Strategies

Modern chargeback prevention requires more than reacting after disputes occur.

The most successful ecommerce brands reduce disputes proactively through operational improvements, payment optimization, fraud prevention, and customer communication.

Use Chargeback Management Tools to Resolve Disputes Early

Card issuers provide tools, like Visa CDRN/Verifi, that send alerts that help merchants resolve disputes before they officially become chargebacks.

Services like Ethoca and Verifi notify merchants when a customer initiates a dispute, allowing businesses to issue refunds or resolve issues before the chargeback formally posts.

This helps merchants:

- Reduce chargeback ratios

- Support healthier VAMP-related monitoring metrics

- Avoid processor penalties

- Preserve merchant account health

Be Transparent About Billing and Return Poicies

Many disputes happen simply because customers don’t recognize transactions. Give your customers the right to make an informed purchase by explaining your subscription policies up front.

Merchants should:

- Use clear billing descriptors

- Communicate return policies ahead of a time

- Send renewal reminders a few days prior to the upcoming billing cycle

- Confirm purchases immediately

- Make cancellation processes accessible

- Communicate billing schedules clearly

U.S. law requires you to inform customers what the “material terms” of their subscription transaction are. Going above and beyond the required disclosures to communicate clearly will decrease the number of purchasers who file chargebacks after being surprised by subsequent charges or automatic renewals.

Reducing confusion significantly lowers friendly fraud exposure.

Set Accurate Expectations Around Your Products and Shipments

Keep customers from claiming your company is withholding products and/or services by clearly communicating what they can expect after making a purchase. Everything from product details to projected delivery dates should be as accurate and as detailed as possible.

Advertise your products honestly (using real photos and videos rather than computer-generated media or product mockups) and check your marketing copy for accuracy. Exaggerating what your product can do may result in disappointed buyers who file chargebacks when the item doesn’t live up to their expectations.

Strengthen Fraud Prevention

Modern fraud prevention requires layered protection.

Effective tools include:

- AI-powered fraud detection and integrations

- Device fingerprinting

- Velocity checks

- 3D Secure authentication

- Behavioral analysis

- Geo-location verification

Fraud prevention should stop bad actors without introducing unnecessary friction for legitimate customers.

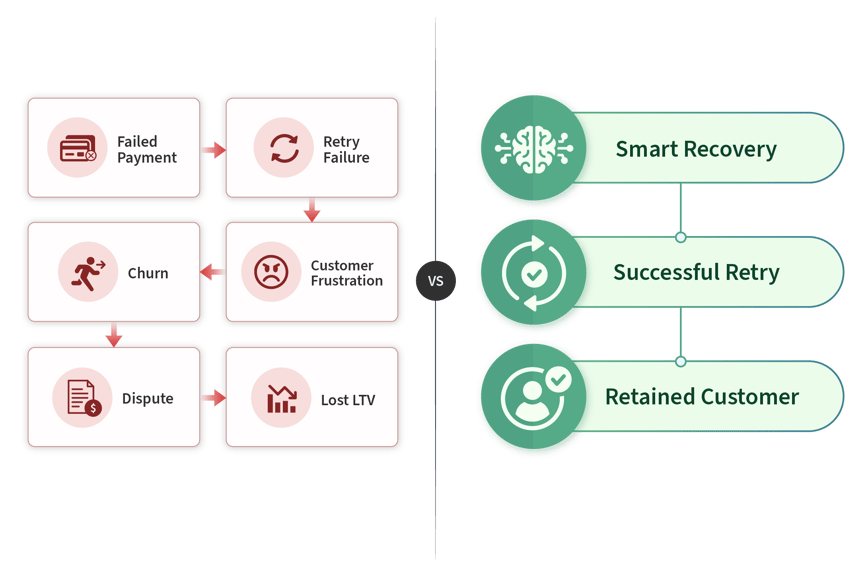

Optimize Failed Payment Recovery

Billing issues and failed payments can contribute to customer confusion, churn, and future disputes if not resolved quickly.

Smart recovery strategies include:

- Intelligent retries

- Account updater tools

- Smart payment routing

- Dunning management

- Automated recovery logic

Recovering failed payments efficiently helps reduce involuntary churn while lowering billing confusion.

Improve Customer Support Accessibility

Customers who can’t quickly resolve issues often escalate directly to banks.

Merchants should prioritize:

- Fast response times

- Self-service cancellation

- Refund visibility

- Multi-channel support

- Transparent policies

When someone reaches out, make sure they know your team is ready to help. Consider automating email responses for each support ticket to acknowledge receipt and set expectations for a response time.

Then, make sure your internal team hits your response time deadlines. According to a survey by SuperOffice, the average response time for email support is approximately 12 hours. That may be out of reach for smaller teams, but we advise you don’t shoot for the upper end of the range in their study (8 days) — that’s plenty of time for a customer to get frustrated and file a chargeback.

Good support experiences can prevent disputes before they begin.

Monitor High-Risk Traffic Sources

Some acquisition channels naturally produce higher dispute rates.

Monitor:

- Affiliate traffic

- Promo abuse

- Fraud-heavy geographies

- Suspicious campaigns

- Abnormal purchasing patterns

Not all growth channels deliver equal customer quality.

How Representments Help Recover Revenue

Even the best prevention strategies can’t eliminate every dispute.

That’s where representments become critical.

What Is a Representment?

Representment is the process of challenging a chargeback by submitting evidence proving the transaction was legitimate.

The evidence required for representment will depend on the chargeback reason. Evidence may include:

- Proof of fraud prevention tools

- Copies of your recurring transaction agreement, plus cancellation and return policies

- Delivery confirmation

- Customer communication

- IP/device data

- Shipping address information, tracking numbers and shipment records

- Usage history

- Subscription acceptance terms

- Refund receipts

- Documentation of merchandise quality and customer satisfaction

Filing and then searching this information manually would be a lot of work. Modern subscription CRMs can help you automate your information storage to save time on this step. Our platform saves customer and transaction information for you and makes it easy to search for the documentation you need.

When Merchants Should Fight Chargebacks

Not every dispute is worth fighting.

Representments make the most sense when:

- Evidence is strong

- Friendly fraud is likely

- Customer usage is clearly documented

- The dispute reason is inaccurate

Strategic representment can help merchants recover revenue and challenge repeat friendly fraud activity.

What Makes a Strong Case

Successful representments rely on documentation and operational visibility.

The strongest cases include:

- Clear terms acceptance

- Product fulfillment proof

- Billing communication history

- Customer engagement records

- Usage logs

- Transaction metadata

Why Automation and Specialist Support Matter

Managing disputes manually becomes difficult at scale.

Automation and specialized represenment experts help merchants:

- Respond faster

- Improve win rates

- Reduce operational strain

- Centralize dispute data

- Scale prevention workflows

Representments shouldn’t be your first line of defense, but they remain an important revenue recovery tool.

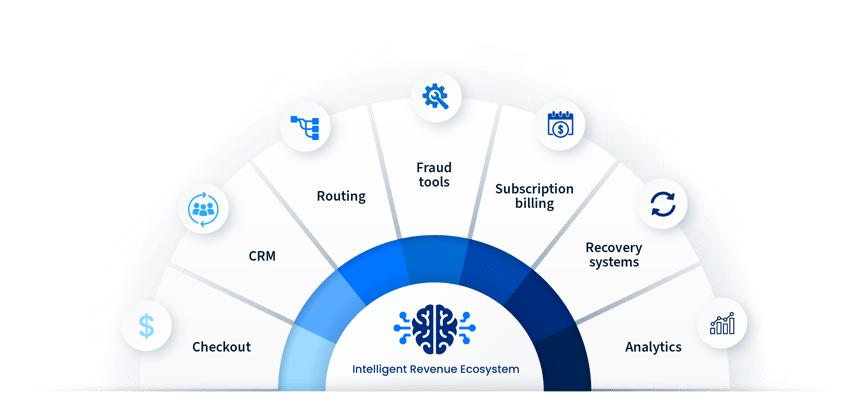

How Smart Payment Infrastructure Helps Reduce Chargebacks

Modern ecommerce brands need more than standalone fraud tools.

Many merchants benefit from connected payment infrastructure that improves visibility across checkout, billing, fraud, recovery, and customer activity.

While fraud tools and alerts help reduce disputes directly, payment optimization tools can also reduce the billing failures and transaction friction that often contribute to customer disputes.

Intelligent Routing Reduces Failed Transactions

Smart payment routing directs transactions toward the processor or acquiring bank most likely to approve them.

This helps:

- Reduce false declines

- Improve approvals

- Lower failed rebills

- Reduce billing-related disputes

Recovery Tools Prevent Revenue Leakage

Automated recovery systems help merchants recover failed recurring payments before customers churn or escalate disputes.

Effective recovery strategies improve:

- Retention

- Customer experience

- Revenue continuity

- Subscription stability

Unified Customer Data Improves Risk Visibility

Connected CRM and payment systems provide better visibility into:

- Customer behavior

- Failed payments

- Refund history

- Dispute and refund trends

- Subscription activity

That visibility helps merchants identify dispute risk earlier.

Why Modern Ecommerce Brands Need Connected Payment Systems

Chargeback prevention no longer exists in isolation.

Today’s ecommerce businesses often rely on multiple connected systems across checkout, billing, recovery, fraud prevention, and customer communication to help reduce operational friction and dispute risk.

The stronger the operational visibility, the easier it becomes to reduce disputes proactively.

Building a Long-Term Chargeback Reduction Strategy

The ecommerce brands best positioned for long-term growth aren’t just focused on acquisition. They’re also protecting the revenue they’ve already earned.

They’re protecting the revenue they’ve already earned.

Long-term chargeback reduction requires:

- Continuous monitoring

- Cross-functional collaboration

- Better customer communication

- Smarter payment infrastructure

- Faster recovery workflows

- Strong fraud prevention

- Operational visibility

The businesses best positioned for growth in 2026 and beyond will be those that treat chargeback management as part of their broader revenue strategy — not just a reactive support issue.