Inflation is soaring, and companies that sell nonessential or luxury goods are likely to take the biggest hit as consumers rethink their spending habits. Merchants looking to prove the worth of their subscriptions should focus on not just price but consumer experience. Research shows that savvy shoppers look for convenience, not just savings when they choose to purchase a subscription.

Convenience, of course, means time saved by automating product deliveries rather than having to make repeat purchases. A subscriber whose delivery is interrupted by failed payments is no longer benefiting from one of the biggest promises of a subscription business. Such an error could spell the end of your relationship with this customer.

Of course, this doesn’t have to happen. Involuntary churn — the type of churn caused by payment failures, also known as passive churn — isn’t the customer’s choice. You have a better chance of winning back its victims than you do the subjects of voluntary churn. It’s a smart choice to focus your efforts on preventing involuntary churn.

Not only does involuntary churn lose money for your company, but it also hurts your reputation with customers and payment processors. That simple truth makes it easy to understand why you should prevent it. But the solution is complex. There are multiple reasons for involuntary churn — you need multiple strategies to combat it successfully.

What Is Involuntary Churn?

Involuntary churn is a blanket term that refers to any subscription cancellations the subscriber didn’t choose to make. This type of churn is caused by payment failures. Because it’s, therefore, a product of customer inaction rather than customer action, it’s also referred to as “passive churn.”

Consumers’ billing information changes when credit cards expire or are reported as lost or stolen. Payments fail when card issuers flag a transaction as fraud or one of your payment service providers experiences an outage.

Some buyers may already be on the fence about canceling their subscription, and the disruption caused by a failed payment is enough to push them over the edge. Others will respond to your requests for updated payment information but would rather not have to deal with the hassle. And, of course, some customers will miss your dunning emails and other communications and simply be surprised when their product doesn’t arrive or when they’re cut off from the service they thought they were paying for.

Voluntary vs. Involuntary Churn

Involuntary churn is a completely different problem than voluntary churn, which refers to customers leaving because they no longer want or need your services. Voluntary churn is a sign of customer dissatisfaction. Buyers may find your prices too steep, product quality not up to their standards or customer support unresponsive, to name a few reasons. In essence, you’ve lost them before the cancellation because they fell out of love with your service.

Involuntary churn, on the other hand, involves customers you haven’t lost in that way. They may love your brand to the point of being an advocate, or they may simply be a satisfied subscriber, but they plan to keep their relationship with your company. The failed payment that causes them to churn is an unwelcome disruption for them in the same way it is for you.

Because involuntary churn affects an entirely different group of customers than voluntary churn does, you can’t address both problems with the same strategy. Your company needs to take steps specifically aimed at preventing involuntary churn if you want to keep your happy customers around for longer.

Why Subscription Sellers Should Care About Involuntary Churn

Involuntary churn is not a small problem. All declined transactions, no matter the cause, have a bigger cost than just the size of the payment. They threaten your relationships with your customers, which is bad for both of you.

When a transaction fails, you get less money (and experience shortened subscriber relationships). Your customers don’t receive the products or services they’re expecting, which could disrupt their lives in multiple ways. And, even if you did your best to fix the problem on your end and communicate with your buyers, the situation is likely to leave a bad taste in their mouths. The end result is either a lost customer or a buyer whose loyalty to your brand decreases thanks to a bad experience.

Finding and Understanding Your Involuntary Churn Rate

Most subscription companies track their churn rates as a whole, but few do the important work of distinguishing voluntary vs. involuntary churn. Distinguishing churn by type may require some manual manipulation of data. However, it’s worth the effort. Your churn reduction efforts won’t be effective if you don’t know what kind of churn is your company’s biggest challenge.

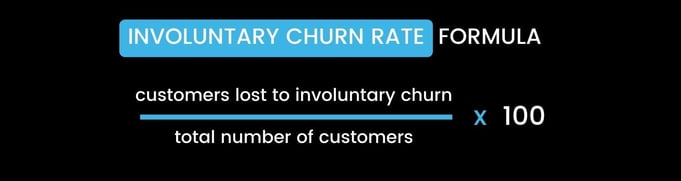

The calculation itself is simple; it’s a variation of the standard churn rate formula. All you need to do is divide the number of customers lost to involuntary churn in a month by your total number of customers, then multiply that result by 100. This formula returns a percentage — your involuntary churn rate.

The bigger challenge is determining how many customers you lost to involuntary churn. The best way to do so is by working with your company’s payment data. Filter your monthly transactions to find those that failed, thereby leading to cancellations (make sure you don’t accidentally include transactions you were able to recover). Alternatively, if your subscription platform adds a reason to customer churn reports, you could filter that data to find buyers who left due to failed payments.

Keep in mind that your involuntary churn rate will never be zero. What you want is a benchmark that you can track as you implement new involuntary churn reduction practices and/or change payment providers. High rates of involuntary churn may be indicative of an issue with your customer onboarding process or subscription software. Failure to collect full or correct billing information will result in high rates of payment failure. Look for unexpected rates of involuntary churn or drastic changes between one month and the next. Either could signal a need to test and/or update your process.

Causes of Involuntary Churn

The first step to fighting involuntary churn is understanding what caused it. There are two types of billing issues your company will need to mitigate: soft declines and hard declines.

Soft declines, or temporary payment authorization failures, are caused by issues like:

- A credit card having insufficient funds

- Charges mistakenly being marked as fraudulent

Such payments often succeed when they’re retried, in which case they don’t become the customer’s problem.

Hard declines happen when the credit card:

- Has expired

- Was canceled after being reported lost or stolen

There’s less you can do to solve a permanent authorization failure like this on your own. Hard declines are typically the trigger for dunning emails or other communications that prompt customers to update their credit card information.

You can learn more about the type of decline you’re facing by looking at the credit card decline code. This two-digit number will let you know why a card issuer refused to complete a payment.

Never be stumped by a credit card decline code again! Download our free Credit Card Decline Codes Cheat Sheet for a guide to the 22 most common codes and tips on how to respond to each.

Credit Card Expiration

It’s hard to imagine anyone has time to sit down and update every single account attached to a credit card when that card expires. Most consumers don’t even remember everywhere they’ve used a particular card. Therefore, you can expect to have a percentage of “card expired” failures every billing cycle.

The transaction failures are hard declines because the account information you have on file is no longer valid.

Closed Account

Credit card accounts may also be closed for fraud, suspected fraud or because a card was reported as lost. As with an expired card, you can expect most customers will forget to change their billing information when their new credit card is issued. And these are likewise hard declines because the account no longer exists.

Incorrect Payment Information

Subscription merchants are less likely to run up against this reason, but you may still see some transactions declined for having incorrect information. In recurring billing scenarios, this is commonly a result of a customer moving; their billing information will change, and if they don’t update it, the credit card issuer will flag the account. You may also see this error arise if a customer mistypes their credit card number (or other payment details) while signing up for a free trial. Because you don’t run the card then, you may not catch the issue until it’s time for their account to become a paid one.

Any account without correct billing information will require a customer’s input before you can retry the payment, as this is another hard decline.

Card Limits Exceeded

Credit card issuers can block transactions based on a consumer’s account limits. A buyer’s credit card may be maxed out, an account may have insufficient funds or a card’s activity limits may be temporarily exceeded on the day you attempt to run a transaction.

These are all examples of soft declines, which means you can attempt the transaction again at a later time. If a card has been paid down, account topped up or enough time has passed since the card’s activity hit the limits, the payment may go through on your subsequent attempts.

Technical Failures

Sometimes, the payment failures are not human errors at all. These days, every payment that’s processed goes through a host of institutions. All of these service providers can fail.

Technical failures may be something as simple as a timeout at any part of the process. Your payment gateway and processor may experience a communication failure, as could any two entities that have to “speak” with each other to send a payment across the web. Sometimes, it’s a one-second failure that happens to catch one of your transactions. Other times, an entire payment processor may go down, causing large batches of payments to fail. This type of payment failure is neither a soft nor a hard decline because the transaction request does not even make it to the credit card issuer.

Transactions can also fail due to card issue system outages. In this situation, a payment request does make it to the issuing bank, but internal errors mean the card issuer can’t respond. This would be a soft decline, so you would simply need to reattempt the payment once the card issuer’s problems are resolved.

Recover up to 75% of failed payments

Enter your email to compare your traditional dunning solution to Smart Dunning!

Credit Card Issuer Discretion

Card brands can choose to block transactions if they believe it’s in their or their customers’ best interests. They don’t want to process payments they believe are fraudulent or otherwise unauthorized by their customers.

Subscription merchants, specifically, may see card issuers decline transactions that aren’t flagged as recurring. Their systems are likely to think these are duplicate charges or otherwise made in error. You’re unlikely to get these transactions through by retrying them unless you also reconfigure your billing software to mark them as recurring payments.

You may also see transactions returned with a “Do Not Honor” or “Transaction Not Permitted” error code. The former is frustratingly nonspecific, and your customer (not you) will need to contact their bank to learn why the payment was declined. The latter is likely due to a consumer attempting a payment with a card brand you don’t accept or in a location their issuing bank doesn’t support. Both of these errors are unlikely to come up on a recurring transaction because the card issuer shouldn’t ever allow the initial transaction in these cases. However, like the incorrect payment information errors, you may see them if you offer free trials and don’t charge a consumer’s card when they sign up.

Why Preventing Involuntary Churn Matters

Fixing involuntary churn is an easy win because neither you nor your customers want it to happen. A low involuntary churn rate means you’re losing less money and disappointing fewer customers than you could be…but it still signifies a loss. Lower revenue and decreased customer lifetime value (CLTV) are only part of the story. Customer acquisition costs are high, and each customer lost reduces your return on the money you spent to win them over. Focusing on customer retention saves resources twice over.

Decline Management Methods to Decrease Your Involuntary Churn Rate

There are multiple causes of involuntary churn, which means your company will need to deploy multiple solutions to fix them. The good news is top subscription software offerings (like sticky.io) address every issue. Many decline management methods can be fully automated, so they won’t even take extra effort on your part. Here are the solutions you should employ if you’re serious about decreasing involuntary churn rates.

Account Updaters Keep Billing Info Current

The best credit card update is one you don’t have to rely on a consumer to do themself. Automated credit card updaters keep the subscription experience seamless without relying on extra effort from your customers. These tools integrate with credit card providers to automatically gather any details — such as the CVV code — that change when a credit card expires.

Account updaters prevent hard declines due to credit card expiration. By doing so, they extend a customer’s subscription length and, accordingly, CLTV. They’re effective, too: 71% of cards that were updated through sticky.io’s Account Updater solution were successfully billed.

Smart Dunning Handles the Problem Before Customers Have To

Consumers sign up for subscriptions because they don’t want to have to think about purchases every month, and Smart Dunning makes that easy. Our automated Smart Dunning tool calculates the best time to retry a failed payment, thereby improving your transaction success rate. AI-powered tools like ours continually gather data over time, learning when a retry will work and when it’s best to ask for customers to manually resolve billing failures. Smart Dunning also protects merchant ID (MID) health by decreasing the number of failed transactions, which means your account is less likely to get shut down by a payment processor — something else that could cause serious involuntary churn.

Automated Dunning Emails Keep Consumers Informed

Billing issues that do need customers’ input should be flagged as early as possible for the best consumer experience. Certain decline codes, like those that indicate incorrect payment information or an account that was closed, will always require your subscriber to update their information. Use these codes as triggers for an automated dunning email sequence. The notifications will empower customers to update their information before the subscription lapses. You’ll also protect your relationship with them by informing them what’s going on so they’re not caught by surprise when a package doesn’t show.

Flexible Subscriptions Make It Easier for Consumers to Pay

A declined payment doesn’t need to be the automatic end of a customer relationship. When you allow subscriptions to be modified month-to-month, customers have more options to keep a subscription active. If their card is maxed, or close to it, downgrading a subscription can be key to keeping it active. Customers whose cards are stolen may appreciate the chance to skip a month while dealing with the hassle of closing their old card and opening a new one.

Your company should also use flexible subscription plans to keep customers around. Try pausing subscriptions after missed payments rather than canceling them. This makes it easier for customers to pick up where they left off, which means they’re more likely to stick with you.

A Good Payment Interface Makes Updating Information Painless

Consumers don’t want to stumble through multiple confusing screens to re-enter payment information. Being asked to update card information is enough of a hassle. A bad user interface leads to a frustrating experience that may result in subscribers entering incorrect payment information or giving up entirely.

On the other hand, a quick and clear process will improve a customer’s overall opinion of your company. So will accepting multiple payment methods: We found 82% of subscribers would like merchants to allow them to pay with their preferred payment methods. Catering to customers’ payment needs will increase the likelihood of keeping their subscriptions active.

Bolster Your Retention Strategy by Preventing Involuntary Churn

Decreasing involuntary churn is one aspect of a larger effort to retain customers. All efforts in this category are especially important during an economic downturn. Consumers are rethinking their discretionary spending, and subscription boxes are a target, given their recurring nature. A missed payment may be the deciding factor for customers who are already on the fence. You don’t want to give anyone a reason to doubt at such a time.

It’s time for ecommerce subscription businesses to be thoughtful about how and where they deploy their resources. Customer churn prevention — and involuntary churn prevention specifically — is a good bet in an economy that’s going to make winning new customers even harder.